Bitcoin Is For Savers. Fiat Is For Debtors.

One of the most common misconceptions in Bitcoin is that “if you don’t spend your bitcoins, Bitcoin will never reach mainstream adoption.” This confuses the sequence of monetary evolution. Every successful money in history first established itself as a store of value before becoming a medium of exchange. People saved gold for centuries before spending it became commonplace. The same pattern applies to Bitcoin. Mainstream adoption begins with people wanting to hold Bitcoin because it preserves purchasing power better than alternatives. Only then does spending naturally follow. The distinction is clear: Bitcoin rewards saving through deflation—its purchasing power increases over time. Fiat punishes saving through inflation—its purchasing power decreases over time. This fundamental difference makes Bitcoin the money for savers and fiat the money for debtors. Which one do you want to be?

Fiat Punishes Savers And Rewards Debt

Inflation destroys purchasing power systematically. At 3-5% annual inflation, prices double roughly every 15-20 years. What $100 buys today will require $200 in two decades. Your savings lose value while you sleep. This isn’t accidental—it’s by design. Inflationary currencies force you to either spend now or gamble in markets to preserve value. Saving becomes irrational behavior. Why would any system punish thrift?

The fiat system requires perpetual debt. Modern economies run on credit expansion. Money is created when banks issue loans; without debt, the money supply contracts. Governments borrow. Corporations borrow. Individuals borrow. The entire structure depends on ever-increasing debt levels. Those who save are outliers swimming against the current. The system is literally built for debtors. How sustainable is an economy that requires infinite debt growth?

Negative real interest rates punish prudence. When inflation exceeds savings account yields, savers lose purchasing power even while earning “interest.” A 2% yield with 5% inflation equals -3% real return. Your bank account grows in nominal terms while shrinking in real terms. The prudent are taxed to subsidize the indebted. Homeowners with mortgages benefit from inflation; savers with deposits suffer. When did saving become a losing proposition?

Hyperinflation destroys savings entirely. Zimbabwe’s hyperinflation reached 89.7 sextillion percent annually in 2008. Prices doubled every 24 hours. Savings worth decades of labor became worthless in weeks. Venezuela, Argentina, Lebanon—hyperinflation isn’t historical curiosity; it’s contemporary reality. In such environments, saving in fiat isn’t just unwise—it’s impossible. The only rational strategy is immediate conversion to hard assets. How many people have lost everything to currency collapse?

Bitcoin Rewards Savers With Increasing Purchasing Power

Bitcoin inverts the fiat incentive structure. Instead of punishing savers, it rewards them. Instead of requiring debt, it enables saving. Its fixed supply of 21 million coins means no one can inflate away your holdings. As adoption grows and supply remains constant, each Bitcoin represents a larger share of the total economic value stored in the network.

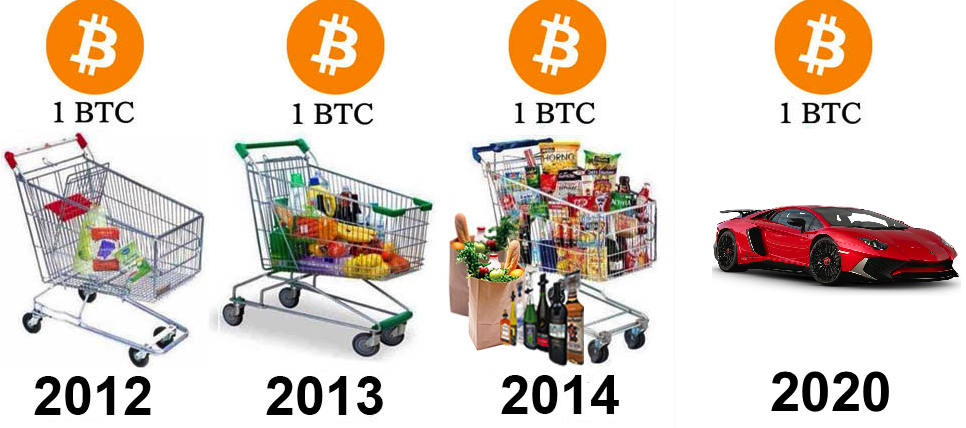

Deflation increases purchasing power over time. As Bitcoin’s value grows relative to goods and services, prices denominated in Bitcoin fall. A car that costs 1 BTC today might cost 0.5 BTC in a few years. Your savings gain purchasing power without you taking investment risks. This is how money should work—rewarding those who defer consumption rather than punishing them. Imagine saving for a down payment while your purchasing power increases rather than erodes.

Fixed supply protects against dilution. Unlike fiat that can be printed infinitely, Bitcoin’s supply schedule is predetermined and unchangeable. No central bank can debase your savings. No government can fund deficits by inflating the currency. Your share of the total Bitcoin supply remains constant regardless of what politicians decide. This predictability makes long-term planning possible again. When did you last feel confident about the future value of your savings?

Savings enables investment and innovation. Economists misunderstand saving. They claim deflation discourages spending and harms growth. But saving isn’t hoarding—it’s deferred consumption that funds investment. When people save Bitcoin, they’re making resources available for productive projects. The Bitcoin ecosystem has grown precisely because early adopters saved rather than spent. Real wealth comes from production, not consumption. What happens when a society values building over spending?

Sound money restores time preference. Inflation forces people to think short-term. Why save when money loses value? Why plan for the future when the future is uncertain? Bitcoin’s deflationary nature encourages long-term thinking. People make better decisions when they can rely on their savings maintaining value. Businesses plan for decades, not quarters. Individuals invest in education, skills, and relationships. Sound money builds civilization; inflation destroys it. How would your decisions change if you trusted your savings?

Bitcoin Is For Savers. Fiat Is For Debtors. Use Bitcoin.

The choice is fundamental. Fiat currency is designed for a debt-based economy. It requires constant spending, perpetual borrowing, and ever-increasing money supply. Savers are collateral damage in this system—their purchasing power sacrificed to keep the debt machine running. Bitcoin offers an alternative. Its fixed supply and deflationary nature reward those who save. Its proof-of-work security ensures no one can change the rules. Its decentralized nature means no one can stop you from holding. Bitcoin is for savers. Fiat is for debtors. This isn’t just economic preference—it’s a choice about what kind of financial system you want to participate in. One that extracts value from the prudent to subsidize the indebted. Or one that rewards patience, planning, and thrift. The world’s savers are discovering Bitcoin. They’re exchanging inflationary fiat for scarce digital gold. They’re opting out of a system that requires their exploitation. You can join them. Build wealth instead of debt. Choose the money that appreciates rather than depreciates. Be a saver. Use Bitcoin.